When I joined Ford, I told the team I wanted to bring an investor’s discipline and a customer’s curiosity to this job. The first quarter of 2026 gave me plenty of both to work with.

We just reported our Q1 2026 financial results, and the headline is simple: Ford is off to a strong start, our products are winning with customers, and we raised our full-year outlook.

Behind that headline number are the people who build, sell, and serve our vehicles every day — through whatever the world throws at us.

And the world has thrown plenty. Last year, Ford absorbed real external shocks — two fires at our largest aluminum supplier, waves of new tariffs and rare-earth export controls, just to name a few.

We’ve called it the “cost of chaos.” It’s not a complaint. It’s the operating environment. And our job is to keep delivering inside it.

Here are the five things I want you to take away from the quarter.

1. Our products are doing the talking.

F-Series is closing in on its 50th consecutive year as America’s best-selling truck. Transit is America’s best-selling van. Explorer is America’s best-selling three-row SUV.

And Mustang? Sales are up 50% — outselling the entire non-premium sports car segment combined.

Put it together, and Ford delivered its highest first-quarter share of U.S. revenue in five years. Customers chose Ford in big numbers, in the segments that matter most.

For me, that’s the most important data point for the first quarter.

2. Revenue is growing — driven by what we build, not by discounting.

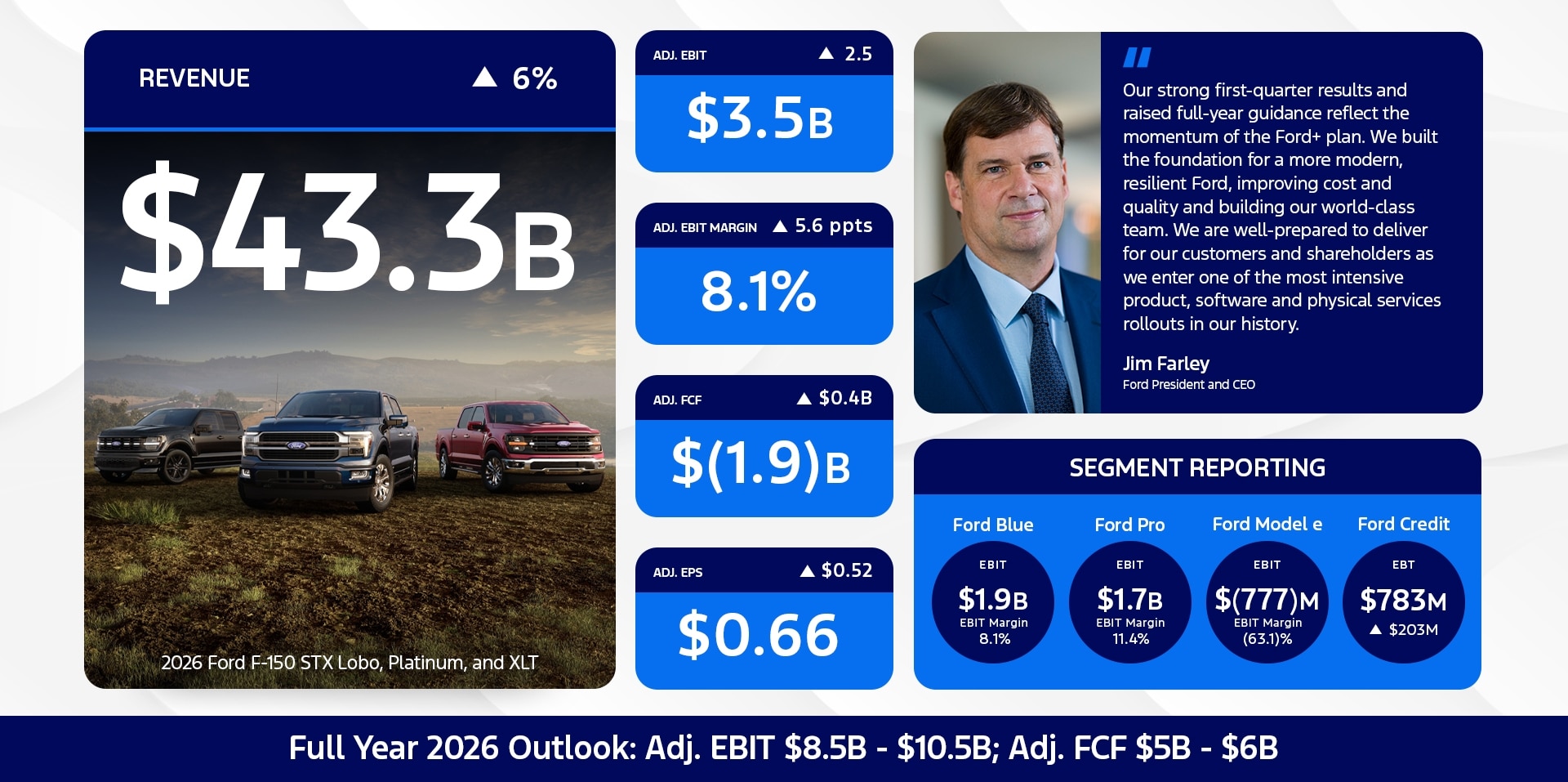

Ford brought in $43.3 billion in revenue in Q1, up 6% from a year ago. We earned $3.5 billion in adjusted EBIT and net income of $2.5 billion.

What I find more interesting than the headline number is how we got there.

Our trucks and large utilities are commanding higher transaction prices, our incentive spend is lower than our key competitors, and our richer mix of off-road trims (Tremor, Raptor, Timberline, Black Diamond) now represents nearly a quarter of U.S. sales.

Translation: we’re growing because customers are choosing Ford — not because we’re paying them to.

I want to be transparent on one item. Our Q1 results recognize a $1.3 billion one-time IEEPA tariff benefit related to tariffs Ford paid between March 2025 and February 2026.

Underlying that, the rest of our adjusted EBIT beat from our prior guidance came from strong product mix and net pricing, as well as continued growth in software and physical services.

3. The cost gap is closing — and that’s structural.

At Ford, we have a commitment to closing our competitive cost gap methodically, quarter by quarter, not through a single dramatic act.

Last year, we delivered $1.5 billion in material and warranty cost reductions — 50% above our $1 billion target. This year, we’re guiding to another $1 billion.

That’s a cumulative $2.5 billion of structural cost taken out. And the work continues.

You can see it in the customer experience. J.D. Power just ranked Ford #4 in its 2026 U.S. Customer Service Index — our best result in nearly 30 years. Warranty costs are coming down. Quality is the foundation of everything: customer trust, dealer profitability, and our long-term margins.

This is the part of the story that compounds. It is not one quarter of noise. It is the cadence we’re building.

4. Ford Pro is the commercial powerhouse of the industry.

In Q1, Ford Pro delivered $1.7 billion in EBIT, up $0.4 billion year-over-year on underlying strength — and that improvement is real, run-rate operating performance.

Our paid software subscriptions hit 879,000, up 30% year-over-year, with software gross margins above 50%. Our parts-and-service attach rate continues to climb toward our long-term target.

This is what a modern commercial vehicle business looks like: hardware that wins on the jobsite, plus software and services that deepen the customer relationship with revenue that recurs every month.

Ford Pro is not a quarter-to-quarter story. It is a structural advantage.

5. We’re investing — and raising expectations.

On the strength of the start, we raised our full-year adjusted EBIT guidance by $500 million, to a new range of $8.5 billion to $10.5 billion, and reaffirmed adjusted free cash flow guidance of $5 billion to $6 billion.

And we have the balance sheet to back it up: $22 billion in cash, $43.1 billion in liquidity, and $18 billion of corporate credit facilities we renewed.

In the quarter, we also repaid our convertible debt without refinancing it and completed an antidilutive share repurchase program. Disciplined capital allocation, every quarter.

Where is that capital going? Into the products that will define Ford’s next chapter. We’re refreshing 80% of our North American portfolio by 2029, including the next F-150 and Super Duty. We’re launching our Universal EV platform in Louisville in 2027 and ramping Ford Energy.

We’re investing through this cycle, and we’re raising expectations, not celebrating. The work outlasts the disruption.

Sherry House is Chief Financial Officer at Ford Motor Company.